The capital markets have suffered a “crude” awakening in March 2026. In this post, we share why pre-IPO planning is the single highest-leverage investment emerging growth companies and their sponsors can make (regardless of which liquidity path they ultimately pursue).

Key Takeaways: Hope is not a Management Strategy

- Pre-IPO planning is not a bet on going public. It is the best way to preserve the greatest number of liquidity options and maximize the value of whichever option you ultimately pursue whether that be IPO, M&A, secondary sale, dividend recapitalization, or otherwise.

- Lack of planning makes everything else harder. Buyers discount unprepared businesses. Bankers cannot move quickly with messy cap tables and unaudited financials. Windows close before you can act.

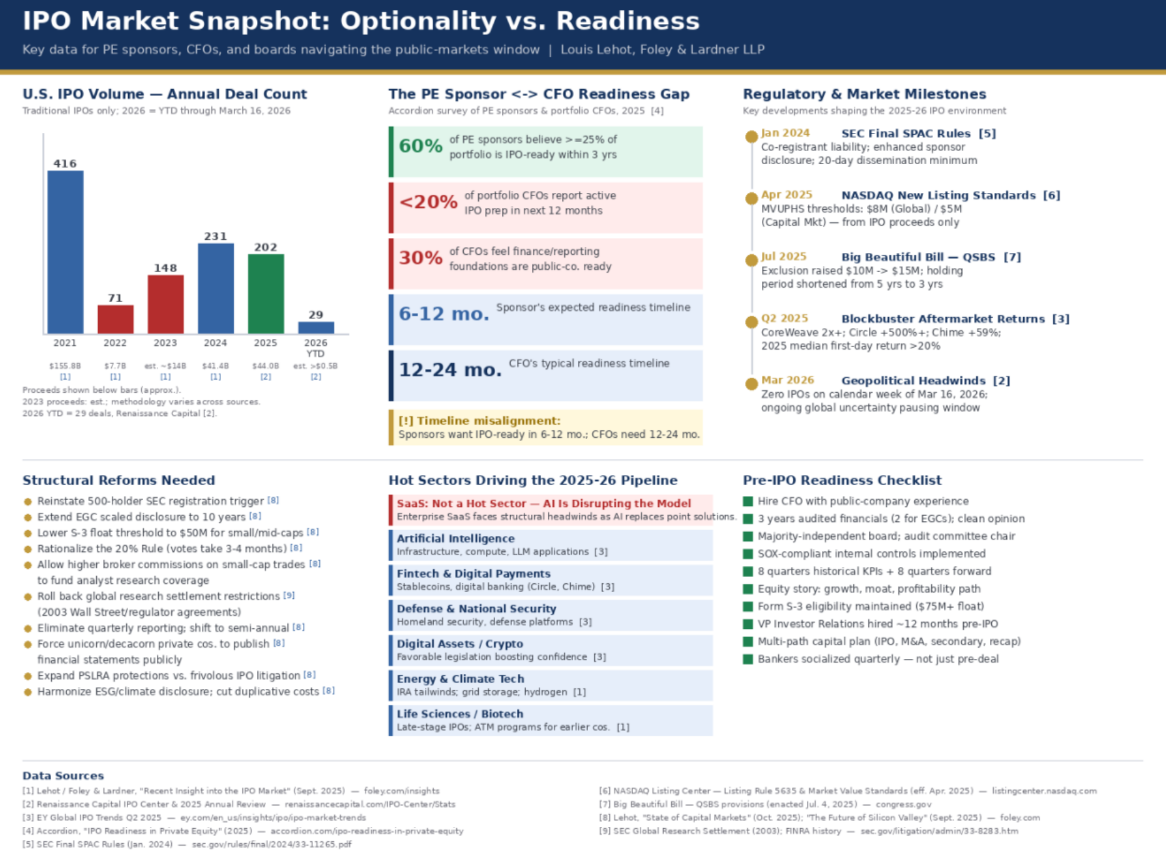

- Accordion’s 2026 survey reveals the scale of the problem: 60% of PE sponsors see IPO potential in their portfolio within three years, yet fewer than 20% of portfolio CFOs are actively preparing. Only 30% feel their finance and reporting foundations are fully public-company ready.

- The regulatory environment has added new complexity: SEC SPAC rules, updated NASDAQ listing standards, and the QSBS overhaul in the Big Beautiful Bill all reshape the landscape for boards thinking about exits.

- Our counsel after 25 years in these trenches: optionality beats perfection, liquidity beats price, and readiness beats hope. The companies that achieve the best outcomes are not the ones that started preparing when the window opened. They never stopped.

There is a question we hear constantly from boards and management teams of PE-backed companies: “Should we start thinking about IPO readiness?” Our answer is always the same, and it surprises some of them. The question is wrong.

Pre-IPO planning is not (or should not be) a decision you make when you decide to go public. It is the foundational work that gives a company the greatest possible chance of achieving the best possible liquidity outcome, whatever that outcome turns out to be. An IPO-ready company is a better M&A target, commands better terms in a secondary sale, qualifies more cleanly for a dividend recapitalization, and has more leverage with lenders and strategic partners across the board. Pre-IPO planning does not narrow your options. It multiplies them. Not doing it does the opposite.

The IPO market of 2025 and early 2026 makes this point vividly. After a four-year high in 2025 where 226 IPOs raised $43 billion, with blockbuster aftermarket returns from CoreWeave, Circle, and Chime, the floodgates were set to open in 2026. But a “crude” awakening has since slammed the window shut. As we write in mid-March, 2026, there are zero IPOs scheduled for the current week. Geopolitical volatility has rattled markets and paused a pipeline that looked robust just months ago. Companies that had been preparing for years are positioned to move the moment conditions stabilize. Companies that had been waiting for the right moment to start preparing are not.

The Gap Is Bigger Than Anyone Wants to Admit

A 2026 Accordion survey of PE sponsors and portfolio company CFOs quantifies a readiness gap that many in the market feel, but few discuss directly. Sixty percent of sponsors believe at least a quarter of their portfolio companies could be prime IPO candidates within three years. But fewer than 20% of those companies’ CFOs report any active IPO preparation underway in the next 12 months. Only 30% feel their finance and reporting foundations are fully public-company ready.

The timeline disconnect is equally stark. Sponsors that are sitting on aging assets with LP pressure building expect portfolio companies to achieve IPO readiness in six to 12 months. CFOs, who must actually implement the transformation, know it realistically requires 12 to 24 months. This is not a small misalignment. It is a structural gap that, unaddressed, will cost sponsors real value when the window opens, and they cannot move.

What created the gap? The IPO market was largely closed from 2022 to 2023. Companies that would have been going public instead pivoted to survival mode: cutting costs, managing debt, and pursuing private financing alternatives. IPO readiness was deprioritized because the market wasn’t going to reward it. That was a rational short-term choice. The long-term cost is that many companies now lack the financial infrastructure, governance structures, and institutional-grade reporting that any sophisticated exit requires (not just a public offering).

Readiness Is the Answer — Whatever the Question

Here is what we tell every board we work with: the question of whether to pursue an IPO is secondary. The primary question is whether your company is the kind of company that can pursue an IPO, because that same state of readiness is what drives the best outcome in every other scenario too.

In an M&A process, a company with two years of clean, audited financials, SOX-compliant internal controls, a majority-independent board, and a well-documented equity story commands a materially better valuation and a faster, lower-friction process than one that does not. Buyers price unprepared businesses at a discount. This is not because of what they find, but because of what they cannot verify. Every week of additional due diligence is leverage in the wrong direction.

In a secondary sale, institutional buyers (e.g., growth equity funds, sovereign wealth vehicles, crossover investors) apply the same scrutiny as a public market investor. They want historical KPIs, forward projections with eight-quarter visibility, a clean cap table, and a management team that understands its own numbers well enough to defend them. A company that has been doing pre-IPO planning has all of this. A company that has not is improvising under pressure.

In a dividend recapitalization, lenders need confidence in the stability and predictability of cash flows. That confidence is built on exactly the same financial reporting discipline and governance infrastructure that IPO readiness requires. And in a strategic partnership or licensing arrangement, the credibility that comes from institutional-grade disclosure and governance is often the difference between a deal that closes and one that does not.

The point is not that every company should go public. Many companies, particularly those with more than $100 million in revenue growing at strong rates with healthy gross margins, have ample private capital available and no compelling reason to absorb the cost and scrutiny of a public listing. The point is that the preparation required to have the IPO as a genuine option is also the preparation that makes every other option better. Pre-IPO planning is not a path. It is a platform.

The Regulatory Environment Rewards the Prepared

The regulatory landscape has added new complexity that makes preparation even more valuable. The SEC’s final SPAC rules, effective July 2024, require target companies to assume co-registrant liability and implement enhanced disclosure requirements. NASDAQ’s updated listing standards, effective April 2025, raised minimum market value thresholds and eliminated the ability to count previously issued shares toward compliance calculations. These changes raise the bar for every company considering a public path and increase the cost of arriving underprepared.

On the positive side, the Big Beautiful Bill signed on July 4, 2025, strengthened the Qualified Small Business Stock exemption, raising the federal tax exclusion from $10 million to $15 million and shortening the qualifying holding period from five years to three. For founders, early employees, and investors who have been building through the difficult markets of 2022 to 2024, this is a meaningful incentive to maintain the long-term orientation that IPO readiness requires. More accommodating merger review at the DOJ and FTC is also improving the M&A environment, which only adds to the argument for having your house in order.

We will be direct about the structural problems that have not been fixed. The U.S. IPO market has averaged approximately 240 deals per year since 2000 — less than one-half of 1990s activity. The number of publicly listed U.S. companies has halved since 1996. Decimalized trading has made it economically irrational for broker-dealers to make markets in smaller-cap stocks. Research coverage of emerging growth companies has withered. These are systemic failures that require systemic reforms, like easing rules that restrict publication of research, enabling brokers to charge larger commissions for facilitating trades in smaller public company stocks, extending “EGC” treatment from five to ten years, lowering the S-3 float threshold, rationalizing the 20% shareholder approval rule and expanding PSLRA protections, to restrictive measures on private companies, like reinstating the 500-holder registration trigger and requiring companies that have raised a billion dollars to publish financial statements. Until those reforms come, companies must work harder to achieve what used to come more naturally. That is an argument for preparation, not against it.

What “File Ready” Actually Looks Like

Being “file ready 365 days a year” is a standard we use with clients, and it is not a metaphor. It means your company can execute a transaction in any form, whether public or private, when conditions are right, without a six-, 12- or 18-month runway to get their house in order first. The elements are straightforward, though the execution is not:

- A CFO with public-company experience who understands the interplay of board oversight, auditor relationships, and investor communication, hired well before you think you need one.

- Two years of audited financials with clean opinions and no material weaknesses. For many PE-backed companies, getting there requires a significant upgrade in the finance function.

- A majority-independent board with an experienced audit committee chair — ideally a former CFO who has navigated a public offering and the ongoing demands of external auditors and regulators.

- SOX-compliant internal controls, a functioning ERP system, and financial reporting infrastructure that can support quarterly public disclosures without heroic effort from the finance team.

- Eight quarters of historical KPIs with documented methodology, plus credible forward projections to the next eight quarters because institutional investors will build models, and those models need to work.

- A compelling equity story that articulates growth trajectory, competitive moat, and path to profitability in terms a public-market investor will accept and that a strategic acquirer, secondary buyer, or lender will find equally credible.

- Form S-3 eligibility maintained at all times. If your public float drops below $75 million, your shelf-takedown capability disappears, and for a mid-cap company caught out of cycle, that can be structurally crippling.

- A general counsel and internal audit function.

None of this is exclusively about an IPO. All of it makes you a better business, a more credible counterparty in any transaction, and a more resilient organization in the face of market volatility. The companies we have watched achieve the best liquidity outcomes, across every form of exit, are not the ones that moved fastest when the window opened. They are the ones that stayed ready through the years when the window was closed.

In 25 years of advising companies from garage to global, this is the clearest pattern we know: preparation is competitive advantage. In a market where the window can close in a week, the companies that keep every option alive are the ones that never stop building toward the one that requires the most discipline to achieve. Not because they will necessarily go public. But because being ready to go public is the best way to ensure that when the moment comes, in whatever form it comes, they are the ones who can move.